The current fight is larger than freedom of navigation at one strait. Iran is trying to turn geography at Hormuz into an acknowledged security role. Israel and its partners are seeking a position near the western gate at Bab al-Mandab. Saudi Arabia and the United Arab Emirates are spending on pipelines and ports that reduce dependence on both gates. Egypt, Turkey, India, China and Russia are backing routes that would redirect trade, data and military access across the same map.

A crisis that has moved beyond Hormuz

On 9 July, tanker movement through the Strait of Hormuz was again close to a halt. Early tracking recorded only two tanker transits, while several vessels reversed course or switched off their automatic identification signals. Three commercial ships had been attacked during the week. One of them, the Qatari liquefied natural gas carrier Al Rekayyat, was left stranded near Oman. War-risk underwriters advised some owners to pause voyages. The shipping response mattered more than the legal question of whether Iran had formally closed the strait. A route can remain open on a chart and still become commercially unusable.[1]

The attacks reopened the dispute that the June memorandum between Washington and Tehran had tried to contain. Iran agreed to permit passage for a limited period, yet Iranian officials maintained that Tehran had not surrendered authority over the route ships would take or the vessels it could inspect. The United States treated unrestricted navigation as the core of the bargain. On 7 July, the US Treasury revoked the general licence that had temporarily authorised transactions involving Iranian oil and replaced it with a wind-down licence. The decision removed one of the few visible economic returns Iran had received under the memorandum.[2][3]

This sequence explains why the argument about Israel and Bab al-Mandab has surfaced now. The United States and Iran are fighting over the rules at the eastern entrance to the Arabian Peninsula. At the same time, Israel, the United Arab Emirates and the United States appear to be improving access on the African side of the Gulf of Aden. Saudi Arabia is examining a further expansion of the pipeline that carries oil to Yanbu on the Red Sea. The UAE is accelerating a second line to Fujairah, outside Hormuz. Maersk and Hapag-Lloyd have begun a cautious return to Suez, even as a fresh attack off Hodeidah showed how quickly confidence can disappear.[4][5][6]

Every government in the area wants an outlet that an adversary cannot shut at reasonable cost. Yet each new outlet depends on another shore, another port and another political agreement. The attempt to escape one chokepoint creates new exposure elsewhere.

Figure 1. The maritime chain around Arabia. Routes are schematic and show the principal strategic connections.

Hormuz and the first contest over rules

Hormuz is narrow, crowded and unusually exposed to land-based force. Iran has the long northern coast, Bandar Abbas and a chain of islands close to the traffic separation scheme. Oman holds the Musandam side and the territorial waters through which part of the internationally used lanes pass. The UAE sits immediately west and south of the strait. Bahrain hosts the US Fifth Fleet, Qatar hosts Al Udeid Air Base, and American forces use facilities across the Gulf. Geography gives Iran the easiest means of disruption, while the United States and its partners have the larger force needed to escort traffic and attack Iranian launch sites.

Iran does not need to seal the passage with a continuous blockade. Mines, missiles, drones, boarding teams and ambiguous attacks can produce the same commercial effect at lower military cost. A handful of incidents may be enough to raise premiums, make crews refuse voyages and leave tankers waiting outside the Gulf. Selective passage is more useful to Tehran than indiscriminate closure. Iran can favour its own exports, exempt politically friendly cargoes, pressure vessels linked to hostile states and offer normal traffic as part of a negotiation. That policy turns navigation into a licensing system without requiring a recognised legal right to administer the strait.

The June memorandum exposed the difference between physical passage and political authority. Washington wanted traffic restored without tolls, harassment or unilateral routing. Tehran read the temporary arrangement as compatible with a continuing Iranian security role. The dispute is about who writes the operating rules after a war.

If Iran gains even informal acceptance that ships need its consent, the result would reach beyond sanctions. Gulf monarchies would have to treat Iranian approval as a recurring cost of export. Insurers and shipping companies would build Iranian political risk into every voyage. The US naval presence would remain large, yet its old promise that the waterway is an international route protected from coercion would be weakened.

Oman has an interest in preventing that outcome without becoming the platform for a war against Iran. Muscat has traditionally used its position on the southern shore to keep communication open with Tehran, Washington and the Gulf states. The same caution shapes the development of Sohar, Duqm and Salalah. These ports give Oman commercial and naval value outside the enclosed Gulf.

Duqm, with its dry dock and access to the Arabian Sea, can host visiting forces without placing them inside Hormuz. Oman gains influence from being the state that can talk to both sides and offer logistics beyond the immediate battle space.

The UAE has chosen a more engineering-heavy answer. Its existing Habshan-Fujairah pipeline moves crude from Abu Dhabi to the Gulf of Oman. During the 2026 disruption, Fujairah allowed the UAE to keep exporting part of its production even when Gulf traffic collapsed. Abu Dhabi has ordered faster work on a parallel line intended to double bypass capacity by 2027.

The limitation is plain. Fujairah is outside Hormuz, but it remains within Iranian missile and drone range. A pipeline changes the loading point. It does not remove the need for air defence, storage protection and secure shipping across the Gulf of Oman.[7]

Figure 2. Hormuz, the Iranian island chain and the ports outside the strait.

The Gulf of Oman and Arabian Sea are the hinge

Once a vessel clears Hormuz, it has not escaped the conflict. It enters the Gulf of Oman, where Iranian ports at Jask and Chabahar face Oman and the UAE. Tankers leaving Fujairah use the same water. Aircraft operating from southern Iran can reach the sea lanes, while ships moving toward India, East Asia or Bab al-Mandab spread across the Arabian Sea.

This wider space is harder to close, but it is well suited to surveillance, shadowing, covert boarding and attacks whose origin is difficult to prove.

The ports on this arc are becoming strategic insurance policies. Fujairah is the UAE outlet. Sohar and Duqm give Oman room for industry and visiting navies. Salalah sits near the western turn into the Gulf of Aden. Chabahar is Iran’s Indian Ocean port and India’s intended gateway to Afghanistan, Central Asia and the International North-South Transport Corridor. Pakistan’s Gwadar, developed with Chinese support, lies farther east and anchors the China-Pakistan Economic Corridor.

None of these ports replaces Suez or Hormuz on its own. Together they create options for cargo transfer, storage, naval replenishment and overland routes that can be activated when the main passage fails.

India sees this area through several overlapping interests. It imports Gulf energy, wants access to Central Asia without crossing Pakistan and cannot allow China to dominate the northern Arabian Sea. Chabahar was meant to connect Indian shipping to Iranian roads and railways running north. US sanctions have repeatedly interrupted that plan. The latest waiver expired in April 2026, leaving the port in legal and financial uncertainty.

At the same time, the Hormuz war pushed India toward more Russian crude and reinforced the value of routes that do not begin inside the Persian Gulf.[8]

China has a different problem. Its energy dependence on Gulf producers is deep, but a large Chinese military role against Iran would damage a relationship Beijing has spent years cultivating. China has preferred to let the United States carry much of the cost of sea-lane protection while Chinese firms build ports, terminals and rail connections.

Gwadar, Djibouti and investments around the Red Sea support commercial access and naval endurance. They also give Beijing evacuation and intelligence options. China can expand these functions without declaring that it will police the route for everyone.

The United States remains the only outside power able to connect operations from Bahrain to Djibouti at scale. Yet the 2026 crisis has shown the burden of doing so. Escorting tankers, defending Gulf bases, intercepting Houthi weapons and retaining strike forces against Iran draw on the same inventories of ships, aircraft and interceptors.

An opponent does not have to defeat the US Navy. It can force Washington to spread expensive assets across a long arc while commercial operators remain free to reroute.

Figure 3. The Arabian Sea, Gulf of Aden and the ports used to approach the western gate.

Bab al-Mandab is a shore war

Bab al-Mandab is often drawn as a single narrow line between Yemen and Djibouti. The military geography is more complicated. Mayun, also called Perim, divides the passage. The Hanish islands lie farther north. Yemen’s western coast contains Hodeidah, Saleef, Ras Isa and Mokha.

On the African side, Djibouti has ports and foreign bases close to the strait, while Eritrea has Assab, Massawa and a long island-studded coastline. Control depends on what happens along these shores and on the political reliability of the authorities that hold them.

The Houthis have the strongest demonstrated denial capability. They control much of northern Yemen and the Red Sea coast around Hodeidah. Mobile missiles, one-way attack drones, explosive boats and coastal surveillance systems allow them to threaten traffic without maintaining a conventional navy.

The attacks since 2023 showed that repeated interceptions do not restore commercial confidence if a few weapons still reach their targets. Western forces shot down large numbers of missiles and drones, yet shipping companies continued to use the Cape route. The attacker chooses the moment. The defender must remain ready through every transit.

Yemen’s anti-Houthi camp does not hold a unified counter-position. Saudi Arabia wants a border settlement, a Yemeni authority that can contain the Houthis and a southern coast that does not become a permanent Emirati sphere. The UAE has relied on local partners in the south and along the coast, including forces associated with the Southern Transitional Council.

Abu Dhabi has valued Aden, Socotra and Mayun as access points in a maritime network. Saudi-Emirati tensions and the UAE’s withdrawal of remaining forces in late 2025 showed that opposition to the Houthis does not produce agreement over the future Yemeni state.[9]

That split limits any campaign to secure Bab al-Mandab from the eastern shore. A coastguard needs a recognised chain of command, functioning ports, radar coverage, trained crews and agreements over arrests and inspections. Yemen has several armed authorities with different foreign patrons.

The Houthis can exploit that division. They can also link maritime attacks to talks over salaries, ports, Saudi security or the war with Israel. Their relationship with Iran gives Tehran influence at the western gate, although the Houthis retain their own interests and may escalate when Iran would prefer restraint.

Djibouti has turned the opposite shore into a market for access. The United States operates Camp Lemonnier. China has its first overseas military support base nearby. France, Japan and Italy maintain facilities. The location covers the strait, the Gulf of Aden, Yemen and East Africa.

Djibouti nevertheless sets political limits on how its territory is used. A base suitable for logistics and surveillance may not be available for offensive operations against Yemen. That gap is one reason Berbera has become more attractive.

Eritrea is the other possible platform. Assab supported Emirati operations during the earlier Yemen war, and its airfield and harbour remain close to Bab al-Mandab. Massawa and the Dahlak islands extend Eritrea’s reach farther north.

Asmara can trade access for money, diplomatic support or security assistance. Its opacity is useful to outside powers, but the political relationship is harder to institutionalise than access in Djibouti. Facilities can be granted quietly and withdrawn just as quietly.

What Israel could actually do from the African side

The claim that Israel is moving toward control of Bab al-Mandab should be read as a forecast of operational access, not a description of sovereignty. Israel has no recognised authority over the strait and no publicly confirmed permanent base there.

Somaliland said in June that Israel was training its police and military but denied talks for an Israeli base. A later report based on satellite imagery and local sources described UAE-led expansion at Berbera airport for possible Emirati, American and Israeli use, including excavations consistent with protected storage and platforms suitable for air defence. The evidence points to a developing access arrangement. It does not prove an Israeli-owned base.[10][11]

Berbera is several hundred kilometres east of Bab al-Mandab, yet distance does not make it irrelevant. Its long runway can support drones, transport aircraft and maritime patrol missions. Fuel, maintenance, communications and protected storage would allow aircraft to remain near Yemen for longer than missions launched from Israel.

Signals-intelligence teams could monitor Houthi communications and Iranian-linked maritime traffic. Radar and electro-optical systems could watch the approaches to the Gulf of Aden. The port could handle logistics, although Berbera is less suitable than Djibouti or Assab for direct control of the narrowest channel.

Israel could combine such access with satellite coverage, long-range aircraft, submarines, naval deployments from Eilat and intelligence supplied by the United States and the UAE. This would shorten the detection-to-strike cycle against missile launchers and drone sites. It would improve warning for ships linked to Israel. It would also give Israel a way to monitor Iranian arms movements around Yemen and the Somali coast.

The military gain would come from persistence. One raid launched from Israel can punish a target. Repeated surveillance from a nearby airfield can map routines, communications and supply chains.

A nearby position would still fall short of sea control. The Houthis can disperse launchers inland, use decoys and fire from a long coastline. Israel has a small navy relative to the space involved. Merchant shipping cannot be escorted vessel by vessel for years at an acceptable cost.

Any Israeli presence would depend on local consent and Emirati or American logistics. It would also make Berbera a target and pull Somaliland into the Iran-Israel conflict. The price Somaliland seeks is recognition and investment. The price it may pay is exposure to attacks, pressure from Somalia and a sharper confrontation with Turkey.

The political return may be larger than the immediate military return. A state that supplies warning, targeting data and defensive technology becomes part of the regional security machinery. Israel can use Red Sea cooperation to deepen quiet ties with Saudi Arabia and Egypt, both of which need the route open.

It can offer the UAE a capable partner for protecting a port network that stretches across the Gulf of Aden. It can also argue in Washington that Israeli access compensates for the restrictions the United States faces in Djibouti.

The Red Sea is no longer one theatre

North of Bab al-Mandab, the route passes several political zones. Yemen and Eritrea shape the southern entrance. Saudi Arabia and Sudan face each other across the central sea. Egypt controls the northern exit. Israel and Jordan sit at the tips of the Gulfs of Aqaba and Eilat.

A ship heading north may pass Houthi launch areas, Saudi energy terminals, Sudanese waters affected by civil war and the Egyptian approaches to Suez. Security at one end cannot compensate for disorder along the rest of the route.

Saudi Arabia has the largest reason to connect Hormuz to Red Sea security. Its East-West pipeline carries crude from the Eastern Province to Yanbu. The system can move about seven million barrels per day in wartime configuration, although part of that volume feeds domestic refineries and export capacity at Yanbu is a separate constraint.

Riyadh is now considering an expansion of as much as two million barrels per day and has discussed access for neighbours such as Kuwait, Bahrain and Qatar. The idea would turn Saudi territory into a collective Gulf escape route.[12]

Yanbu solves only half of the problem. Cargo for Europe can sail north to Suez. Cargo for India and East Asia must sail south through Bab al-Mandab. A simultaneous crisis at Hormuz and the western gate would strip much of the value from the Saudi bypass for Asian customers.

The kingdom therefore needs a stable Yemeni coast, effective air and missile defence around the Red Sea and a working relationship with Egypt. It also needs to keep the route from becoming an Israeli-Iranian battle line that Saudi Arabia cannot control.

Saudi projects at NEOM and along the north-western coast add another layer. They assume that the Red Sea can support tourism, industry, data cables and new cities. Persistent missile risk would raise financing and insurance costs far beyond shipping. For Riyadh, maritime security is tied to the credibility of its domestic development programme.

Sudan creates a different uncertainty on the western shore. Port Sudan is the main gateway for the army-held part of the country. The civil war has drawn in Egypt, the UAE, Iran and other outside actors.

Russia has kept alive an agreement for a naval logistics facility, although instability and attacks near the coast make construction uncertain. A Russian presence would not close the sea. It would give Moscow a resupply point between the Mediterranean and Indian Ocean, a platform for intelligence and another bargaining asset with Egypt, the Gulf states and the United States.[13]

Eritrea has more usable geography and fewer institutional restraints. Djibouti has better infrastructure and many foreign partners, but it protects its freedom of action by balancing them. Sudan has scale, ports and a route into the African interior, but war limits its reliability.

Outside powers are spreading their access rather than trusting one coast. The result is a dense belt of small facilities, training missions, commercial terminals and dual-use airports.

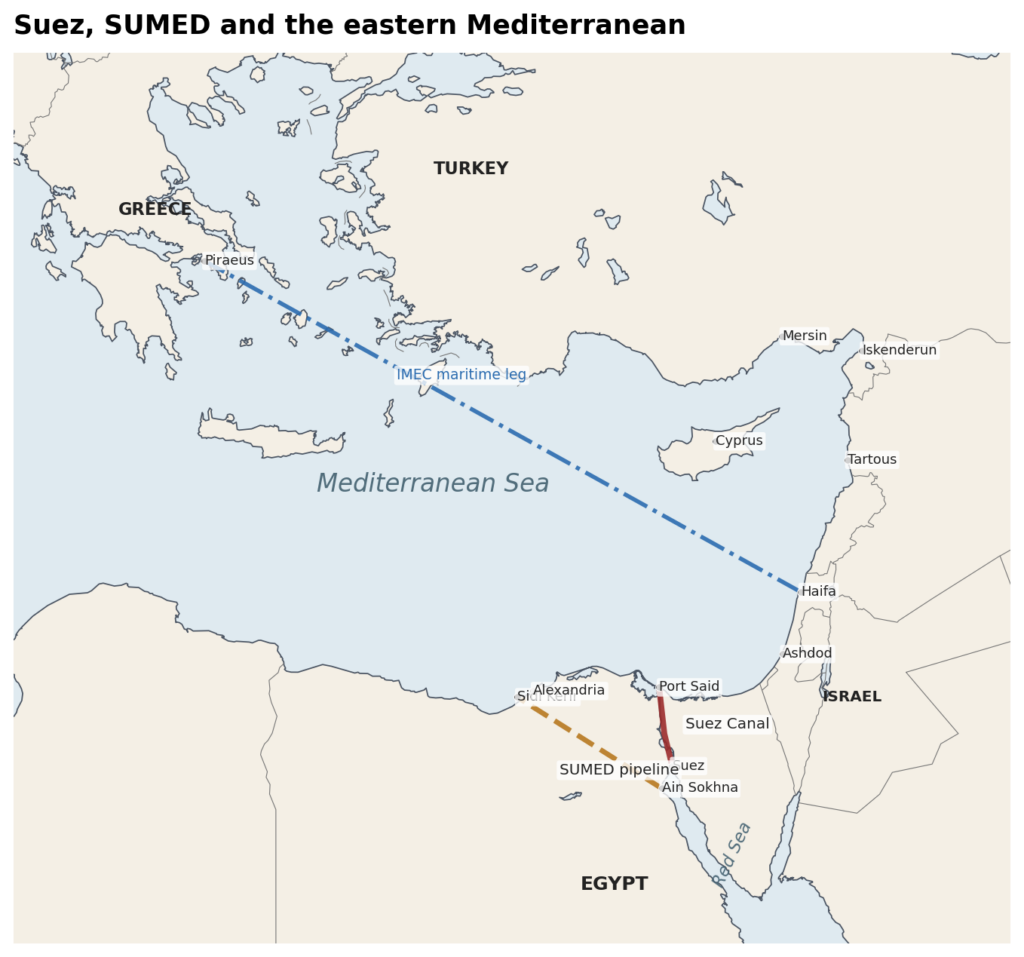

Figure 4. The Red Sea links Saudi bypass exports, Israeli access, African bases and the Suez route.

Suez, SUMED and the northern exit

Egypt earns transit revenue at the northern end of a route whose security is decided far to the south. The Suez Canal can operate perfectly and still lose traffic if owners fear Bab al-Mandab. The Houthi campaign forced container lines around the Cape of Good Hope and cut Egyptian receipts.

The return of Maersk and Hapag-Lloyd services in July is an economic relief, but it remains a trial rather than a final restoration. Maersk estimated that the Suez route would cut some voyages by seven to fourteen days compared with the Cape diversion.[4]

The SUMED pipeline gives Egypt a second function. Crude arriving at Ain Sokhna on the Red Sea can cross Egypt to Sidi Kerir on the Mediterranean. Its capacity is about 2.5 million barrels per day.

SUMED can handle cargoes that are too large for a fully loaded canal transit and can keep some oil moving if canal operations are constrained. Like the canal, it depends on tankers reaching the northern Red Sea in the first place.[14]

Cairo has three concerns about the growing foreign presence farther south. It wants Saudi exports and Asian-European trade to return to Suez. It does not want Turkey, the UAE or Israel to dominate the Horn of Africa. It also sees Ethiopia’s search for sea access through the lens of the Nile dispute.

Egyptian policy therefore combines naval cooperation with Saudi Arabia and the United States, support for Somalia’s territorial position and caution toward arrangements that would strengthen Somaliland or Ethiopia.

The eastern Mediterranean connects the maritime contest to another set of ports and rivalries. Haifa and Ashdod are possible western nodes for the India-Middle East-Europe Economic Corridor. Piraeus is a Chinese-operated gateway into Europe. Turkey has Mersin, Iskenderun and the overland route from Iraq and the Caucasus.

Syria offers Tartous and Latakia, where Russia and the UAE are competing for commercial and military influence. Cyprus is a potential energy and cable node. The route that emerges from Suez enters a crowded market rather than a neutral European approach.

Figure 5. The canal, SUMED and the ports competing for the northern end of the route.

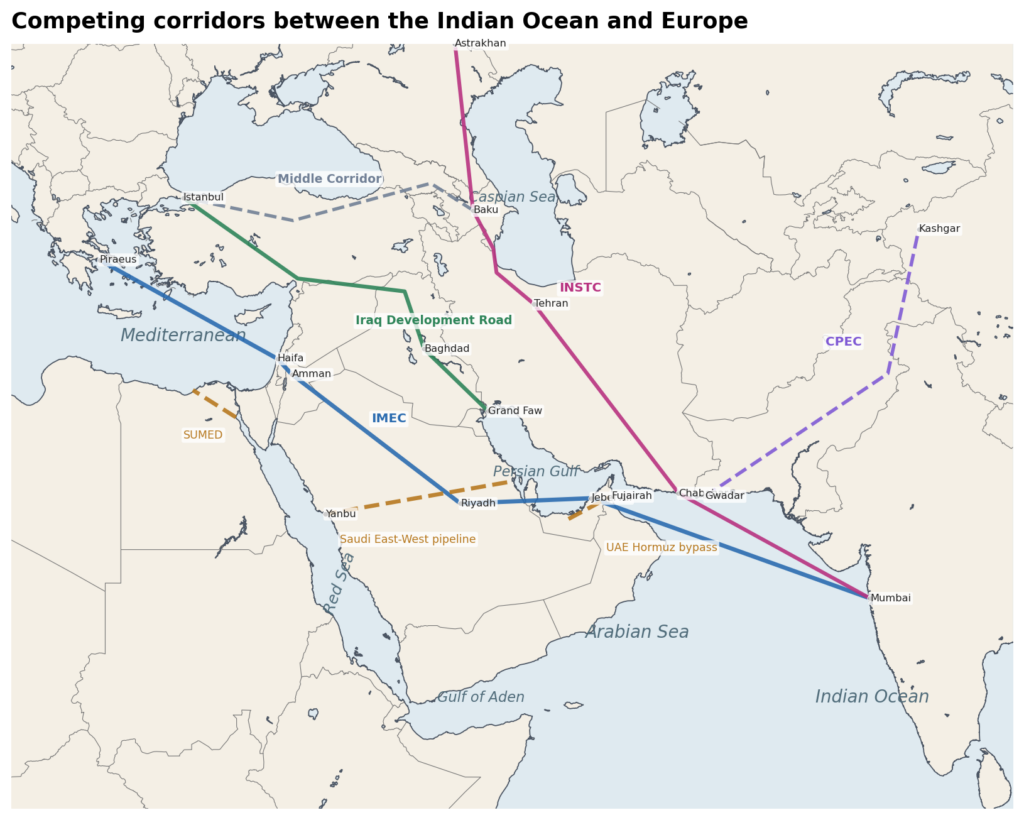

The corridor contest is the landward side of the same war

The region’s corridor projects are usually advertised as trade initiatives. Their strategic purpose is to reduce dependence on hostile water and bind partner states into long-lived infrastructure.

Railways, pipelines, electricity lines and data cables distribute risk differently from shipping. They also create fixed nodes that can be pressured, sanctioned or attacked. No project eliminates geopolitics. Each chooses a different set of states through which the risk will run.

The Saudi and Emirati bypasses

The Saudi East-West pipeline and the UAE lines to Fujairah are the only large bypasses already capable of moving Gulf crude at scale. They are short in political terms because they remain inside one state. Their weakness is terminal concentration.

Yanbu must be protected from attacks across the Red Sea. Fujairah is exposed to Iran from across the Gulf of Oman. Expanding pipe capacity without loading berths, storage, air defence and a secure onward sea route would create impressive nominal numbers with limited wartime throughput.

Saudi discussions with Kuwait, Bahrain and Qatar point toward a larger change. If neighbours obtain access to Saudi pipelines, Riyadh becomes the transit state for part of their energy trade. It gains fees and political weight.

Those states gain an outlet, but their exports become dependent on Saudi infrastructure and pricing. The project would alter relations inside the Gulf Cooperation Council as much as it would reduce Iranian leverage.

IMEC and the Israeli-Saudi route

The India-Middle East-Europe Economic Corridor proposes a maritime leg from India to the UAE, a rail crossing through Saudi Arabia and Jordan to Israel, and a second sea leg to Europe. Its appeal is clear during a Red Sea crisis: container traffic could avoid Bab al-Mandab and Suez.

A version using Omani ports could also reduce reliance on Hormuz. The corridor could carry electricity, hydrogen and data alongside freight.

Its political requirements are severe. Goods must cross several customs systems and transfer between ships and rail at least twice. The Saudi-Israeli connection depends on a political relationship that remains vulnerable to the Palestinian conflict. Jordan would become a transit state exposed to domestic opposition and regional pressure.

Israel’s ports and railways would be military targets during a wider war. Egypt sees the project as a possible competitor to Suez and has linked progress to a settlement of the Palestinian issue.[15]

The route should be understood as a bargaining project before it becomes a high-volume transport system. It gives India, the UAE and Saudi Arabia a framework for standards and investment. It gives the United States a corridor that excludes Iran and competes with Chinese infrastructure.

It gives Israel a reason to be included in Gulf trade even without a comprehensive regional peace. Its strategic effect begins before the rail gaps are closed because governments make port, cable and customs decisions in anticipation of it.

Iran, Chabahar and the north-south route

The International North-South Transport Corridor links Indian Ocean shipping to Iran, the Caspian basin, Russia and northern Europe. Cargo can enter through Bandar Abbas or Chabahar, move by road and rail toward Tehran and Rasht, then continue through Azerbaijan or across the Caspian.

The route allows India to reach Eurasia without Pakistan. It also gives Iran a transit role that does not depend entirely on oil exports through Hormuz.

Sanctions are the route’s central vulnerability. Banks, insurers and logistics firms may avoid Iranian nodes even when the physical infrastructure exists. Chabahar has received temporary exemptions because of its connection to Afghanistan, but the waiver cycle prevents normal long-term finance.

War adds a second problem. Ports outside Hormuz are safer than Gulf terminals, yet they remain part of Iran’s strategic rear and can be targeted. Iran can offer geography, but it cannot separate that geography from its confrontation with the United States.

The Iraq Development Road and the Turkish route

Iraq’s Development Road is planned from Grand Faw port through Baghdad to Turkey and Europe. Iraq, Turkey, Qatar and the UAE signed a cooperation agreement in 2024. The project competes with Suez for some Asia-Europe cargo and with Iran for north-south transit.

It also gives the UAE a route that reaches the Mediterranean through friendly investment relationships rather than Israel.[16]

Grand Faw lies inside the Gulf and therefore remains exposed to Hormuz. The project can shorten the overland segment once goods arrive, but it cannot solve a closure at the eastern gate unless cargo first reaches an outside port and is transferred into the Iraqi network.

Iraq is studying new oil-export pipelines as well, which reflects the same search for options after the 2026 disruption.[17]

Turkey wants the Development Road because it would draw Gulf trade north through Turkish territory and reduce the importance of routes crossing Iran or the Caucasus without Turkish control.

Ankara’s position in Somalia adds a maritime dimension. Turkey trains Somali forces, has a large military facility in Mogadishu and agreed to support Somalia’s maritime security. It opposes Israeli recognition of Somaliland and does not want Berbera to become an Israeli-UAE military node beyond Mogadishu’s authority.[18]

China’s port chain and the Middle Corridor

China is present on both sides of the system. Gwadar connects the Arabian Sea to western China in theory, although terrain, security and cost prevent it from replacing maritime trade. Piraeus gives Chinese firms a major Mediterranean foothold. Djibouti supports naval deployments and commercial logistics.

The Middle Corridor across Central Asia, the Caspian, the Caucasus and Turkey offers another way to reach Europe without Iran or Russia, but it has capacity and coordination limits.

Beijing benefits from a network in which no single American-controlled passage can stop Chinese trade. It also benefits when regional states spend their own money on ports and railways.

China is unlikely to choose one exclusive corridor. It will invest across several and seek commercial terms that preserve access under different political alignments.

Data routes are joining the competition

The struggle is no longer confined to oil and containers. An Iraqi-Emirati consortium announced the WorldLink project in February 2026, with a subsea cable from the UAE to Faw and an overland route to Turkey. Saudi Arabia and Syria have discussed a separate fibre link.

IMEC documents include digital cables and power connections. Subsea systems through the Red Sea and Suez already carry a large share of communications between Asia and Europe.[19]

Data cables change the value of ports and landing stations. A port with power, protected cable landings, cloud infrastructure and military communications can support both commerce and intelligence. It also becomes a target for sabotage or coercive regulation.

States that host several routes can sell resilience. States dependent on one landing area can be pressured without a ship ever being attacked.

Figure 6. The principal pipeline, rail, port and overland projects competing across the same geography.

What each power is trying to obtain

Iran wants recognition that its proximity to Hormuz produces political authority. The most favourable outcome for Tehran is a managed passage regime in which shipping continues, Iranian exports receive sanctions relief and the United States accepts limits on military operations near the strait.

Iran also wants the Houthi threat to remain available at Bab al-Mandab, since pressure at the second gate complicates every Gulf attempt to bypass the first. Tehran must calibrate this pressure. A complete and prolonged shutdown would accelerate pipelines, alternative ports and political coalitions designed to exclude Iran.

Israel wants to prevent the Houthi front from becoming a permanent veto over Eilat and Israeli-linked shipping. Access around Berbera would improve surveillance and strike endurance. The larger objective is admission into the security arrangements that protect Saudi, Emirati and Egyptian trade.

Israel gains political value when Arab governments need its sensors, air defence or intelligence even if formal normalisation is stalled.

Saudi Arabia wants a western export system that remains under Saudi influence. It needs Yanbu, Suez and Bab al-Mandab to function together. Riyadh also wants to stop the UAE from converting its port network and local partners into a position that outflanks Saudi influence in Yemen and the Horn.

The kingdom may cooperate with Israel quietly against Iran and the Houthis, but it will resist an Israeli role that appears to supersede Arab control of the Red Sea.

The UAE wants multiple doors. Fujairah gives it an outlet outside Hormuz. Berbera, Bosaso and earlier access at Assab have extended its reach around the Gulf of Aden. Investments in Grand Faw and the Development Road connect it to Turkey. Participation in IMEC connects it to India, Saudi Arabia and Europe.

Abu Dhabi’s method is to combine port concessions, commercial operators, security training and local political relationships. The model produces flexibility, though it also causes friction with Saudi Arabia, Somalia and Turkey.

Egypt wants traffic back in Suez and foreign military activity kept far enough from its own strategic autonomy. It will cooperate with navies that help reopen the route, but it has little reason to welcome a corridor architecture that bypasses the canal or an Israeli position in Somaliland that strengthens Ethiopia and weakens Somalia.

Cairo’s Red Sea policy is tied to the Nile, Sudan and the balance with Turkey.

Turkey wants Somalia’s coast, the Development Road and its Mediterranean ports to form a Turkish-centred route between the Gulf and Europe. It sees Somaliland recognition as a precedent that could fragment a partner state and give Israel and the UAE access near Yemen.

Turkey can answer with military support to Mogadishu, economic ties with Ethiopia and promotion of the Iraqi route.

The United States wants open passage without becoming the permanent escort service for every commercial vessel. It also wants corridors that connect India, the Gulf and Europe while limiting Chinese and Iranian control.

Washington is likely to support dispersed allied access in Berbera, Duqm, Djibouti and the Gulf. The difficulty is that local partners have conflicting agendas. A network built to contain Iran can also sharpen Saudi-UAE, Turkish-Emirati and Somali-Somaliland disputes.

Europe wants Suez restored, energy prices contained and a defensive maritime role that does not lead to an open-ended war in Yemen. The EU extended Operation Aspides to February 2027. Its area covers the Red Sea and surrounding waters, with a defensive mandate focused on vessel protection and maritime awareness.

That mission helps commercial traffic, but it cannot remove launch sites on land or settle the political conflicts that generate attacks.[20]

India wants supply security and access to Eurasia. It has reason to support IMEC, Chabahar and the north-south route at the same time. These projects are competitors on a map, yet for India they are insurance against different failures.

New Delhi will avoid choosing between Iran, Israel and the Gulf states unless sanctions or war force the choice.

The outcomes now taking shape

The most probable near-term condition is unstable passage rather than a settled closure. Hormuz traffic will rise after negotiations and fall after attacks. The Red Sea will reopen service by service, with carriers retaining the Cape option.

Insurance pricing will react faster than diplomacy. This gives Iran and the Houthis leverage even when they do not sustain a high tempo of attacks.

The second outcome is a construction cycle. Saudi Arabia will push more capacity toward Yanbu and may offer pipeline access to neighbours. The UAE will finish the second Fujairah line and add storage and air defence. Oman will market Duqm, Sohar and Salalah as ports outside the Gulf confrontation.

Egypt will adjust canal fees and work with carriers to restore Suez traffic. Berbera and Bosaso will attract further military and logistics investment because foreign governments want alternatives to Djibouti.

A quiet Israeli presence near the Gulf of Aden is more likely than a declared base. Training, intelligence teams, temporary aircraft deployments, radar sharing and use of Emirati facilities provide much of the operational value without the diplomatic cost of an Israeli flag over a permanent installation.

Somaliland can deny a base while permitting cooperation. The arrangement will remain vulnerable to exposure, local politics and attacks.

Yemen will remain the point at which expensive naval power meets cheap coastal weapons. Unless there is a political settlement that includes port control and a security arrangement for the western coast, the Houthi threat will survive air strikes.

The movement does not have to dominate the sea. It needs enough weapons and uncertainty to keep shipping decisions political.

Corridor competition will intensify, but none of the headline projects will replace Suez or Hormuz in the next few years. Pipelines can reroute a share of oil. Rail corridors can take high-value and time-sensitive cargo. Data cables can bypass contested landings. Bulk trade will continue to rely on ships.

The practical result will be a more expensive network with extra storage, duplicated infrastructure and spare routes that are used intermittently.

The dangerous scenario is a coordinated two-gate crisis. If Iran sharply restricts Hormuz while the Houthis resume sustained attacks at Bab al-Mandab, Gulf exporters lose both the direct route and much of the value of the Red Sea bypass.

US and European forces would have to protect two operational areas. Saudi Arabia would face pressure at the end of its pipeline. Egypt would lose Suez traffic. Israel would expand strikes on Yemen. Facilities in Berbera, Djibouti, Assab and the Gulf could become targets.

Even a short episode would accelerate the division of the region into rival maritime blocs.

A cooperative regime for Hormuz remains possible in theory. It could begin with notification rules, incident hotlines, common navigation standards and environmental cooperation between Iran, Oman and the Gulf states.

This is the logic behind comparisons with early European integration. The present military balance works against it. The parties still believe that control of insecurity gives them more leverage than shared management. The first durable agreements are more likely to be technical and narrow than supranational.

The map that is emerging

Israel cannot own Bab al-Mandab, and Berbera cannot by itself deliver control. What Israel can seek is a place inside the system that watches and contests the strait.

That position would connect Eilat, long-range air power, US naval coverage, Emirati access and African facilities. Its purpose would be to deny Iran and the Houthis a free hand at the western gate and make Israel useful to the states whose pipelines and canal revenues depend on that gate.

Iran is pursuing the mirror image at Hormuz. It wants international shipping to accept that passage is physically possible but politically conditional. Saudi Arabia and the UAE are building around that claim with pipelines and ports. Egypt is defending Suez. Turkey is backing Somalia and the Iraqi route. China is spreading investments across several systems. India is keeping options open in rival corridors.

The region is moving away from one protected sea lane toward a network of guarded routes. The strongest actor will not be the state that closes a strait forever. It will be the state, or coalition, that can interrupt an opponent’s route while keeping enough alternatives open for its own trade.

That is the meaning behind the warning that attention fixed on Hormuz may miss the shift at Bab al-Mandab. The two gates are now being contested together.

Source notes

- Reuters, “Oil tanker traffic through Hormuz at near standstill as attacks strain Iran truce,” 9 July 2026. Source

- US Treasury, OFAC, “Issuance of Amended Iran-related General License,” 7 July 2026. Source

- Reuters, “Iran insists on keeping control over Hormuz, senior Iranian sources say,” 1 July 2026. Source

- Reuters, “Maersk to resume Middle East-US East Coast shipping through Suez Canal,” 9 July 2026. Source

- Reuters, “Saudi Arabia considers expansion of oil pipeline to Red Sea, sources say,” 7 July 2026. Source

- Associated Press, “British military says cargo ship reports attack in the Red Sea off Yemen,” 5 July 2026. Source

- Reuters, “UAE to accelerate oil pipeline project to help bypass Hormuz,” 15 May 2026. Source

- Reuters, “US grants India six-month sanctions waiver to run Iran’s Chabahar port,” 30 October 2025. Source

- Reuters, “UAE to pull remaining forces from Yemen in crisis with Saudi Arabia,” 30 December 2025. Source

- Reuters, “Somaliland receiving Israeli military training but not in talks for base, minister says,” 17 June 2026. Source

- Le Monde, “UAE discreetly builds military base in Somaliland for US and Israel,” 6 July 2026. Source

- International Energy Agency, “Strait of Hormuz: oil security and emergency response,” 2026. Source

- Reuters, “Russian Red Sea base deal still on the table, Sudanese foreign minister says,” 12 February 2025. Source

- US Energy Information Administration, “Red Sea chokepoints are critical for international oil and natural gas flows,” 4 December 2023. Source

- Reuters, “Egypt says resolving Palestine issue is key for progress in India-Europe transit corridor,” 17 October 2025. Source

- Reuters, “Iraq, Turkey, Qatar, UAE sign preliminary deal on Development Road project,” 22 April 2024. Source

- Reuters, “Iraq approves preliminary agreements to study strategic oil export pipeline projects,” 5 July 2026. Source

- Reuters, “Turkey to provide maritime security support to Somalia,” 22 February 2024. Source

- Reuters, “Iraqi-UAE consortium plans $700 million fast data cable network,” 16 February 2026. Source

- Council of the European Union, “Red Sea: Council extends the mandate of Operation ASPIDES,” 23 February 2026. Source

- US Energy Information Administration, “Global Energy Security Data,” 2026. Source

- Combined Maritime Forces, “CTF 153: Red Sea Maritime Security,” accessed 9 July 2026. Source

The maps are analytical schematics. Routes show strategic direction and principal nodes rather than surveyed alignments or recognised maritime boundaries.